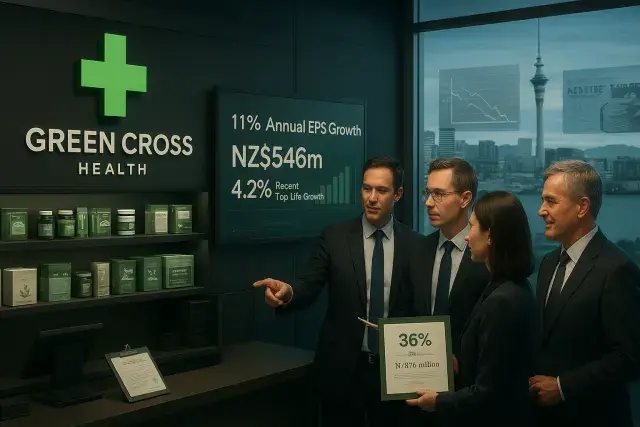

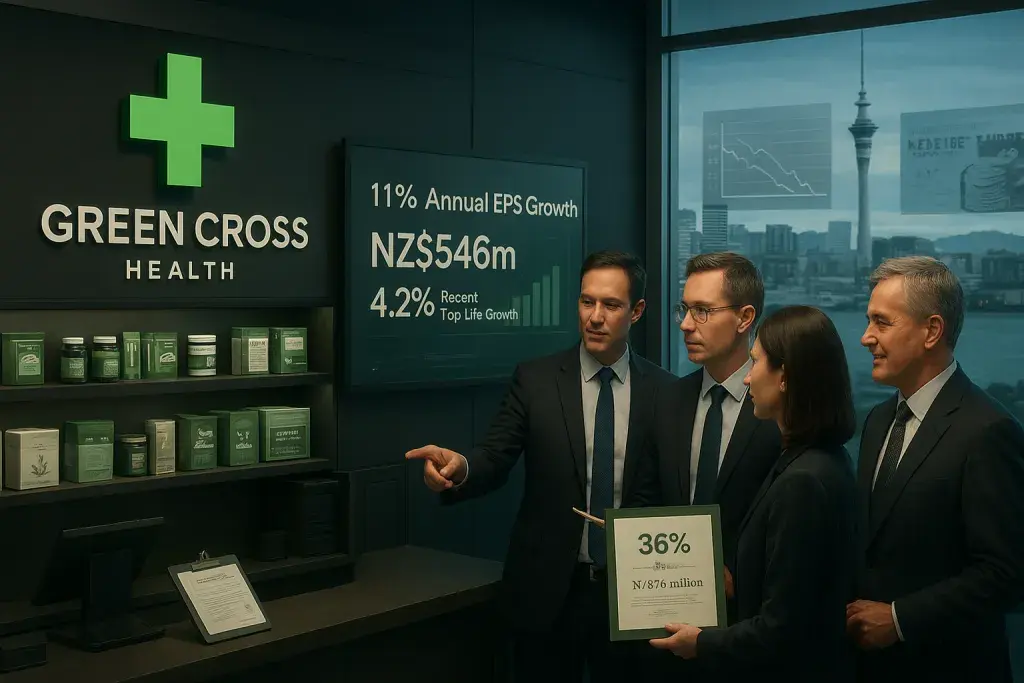

Profitability is a rare and underappreciated asset in regulated cannabis retail - and Green Cross Health (NZSE: GXH) is making a credible case for why it matters. The New Zealand-listed operator has grown earnings per share at roughly 11% annually over three years while posting revenue of approximately NZ$546 million, with top-line growth of 4.2% in its most recent reporting period. For investors and operators watching the broader licensed cannabis market, the numbers are worth understanding in context.

The Profitability Problem Most Cannabis Operators Haven't Solved

Here's the thing about cannabis retail at scale: the cost structure is punishing. Between excise tax obligations, compliance overhead, inventory management, and the operational drag of seed-to-sale tracking requirements, many licensed operators run thin margins even when revenue looks impressive. A company that can grow EPS consistently while holding its EBIT margin steady - as Green Cross Health has done - is doing something that most multi-state operators in North American markets have struggled to replicate.

Peter Lynch's old observation, that "long shots almost never pay off," reads differently when you're looking at regulated retail rather than speculative tech. Cannabis businesses are capital-intensive. Buildouts, licensing fees, compliance software, POS system integrations, and compliant packaging requirements eat into working capital before a single product hits the budroom floor. A company that is burning cash and telling a good story can sustain that position for years - right up until it can't. Profitability isn't glamorous. It is, however, durable.

Insider Ownership as an Operational Signal

Green Cross Health's insider ownership stands at approximately 36% of shares outstanding, with the value of those holdings sitting around NZ$78 million at current prices. That level of alignment matters beyond the standard corporate governance argument. In cannabis retail specifically - where regulatory scrutiny is high, licensing conditions can shift quickly, and compliance failures carry real consequences - operators whose leadership has meaningful personal financial exposure tend to run tighter ships. They have skin in the outcome of every compliance audit, every inventory reconciliation, every wholesale pricing decision.

That's not a guarantee of good management. But it's a reasonable signal that the people running the business aren't indifferent to how it performs. In a sector where executive turnover has historically been high and short-term capital raises have sometimes obscured underlying operational weakness, insider alignment is worth weighting accordingly.

What Sustainable Revenue Growth Actually Looks Like in Licensed Retail

The 4.2% revenue growth Green Cross Health recorded might look modest against the growth narratives that have circulated in cannabis markets over the past decade. Fair enough. But context matters here. Many cannabis operators in adult-use markets posted explosive top-line numbers in early licensing periods - driven by limited competition, novelty demand, and temporarily elevated wholesale pricing - only to see those numbers compress sharply as markets matured, license caps lifted, and per-gram pricing fell.

Steady, margin-stable revenue growth in a regulated retail environment tells a different story. It suggests pricing discipline, controlled SKU management, and a supply chain that isn't lurching between oversupply and shortfall. For dispensary operators and their wholesale partners, that kind of predictability is operationally valuable - it keeps inventory shrinkage down, supports reliable delivery manifest planning, and makes compliance logging less chaotic.

Green Cross Health's market capitalization of NZ$216 million keeps it in small-cap territory. That size brings its own considerations - balance sheet resilience, access to credit, and capacity to absorb regulatory changes without destabilizing operations are all worth examining closely at that scale. But small doesn't mean fragile, particularly when profitability is real and insiders are invested in protecting it.

The Broader Lesson for Cannabis Business Investors

The cannabis industry has produced no shortage of compelling stories attached to loss-making operators. Vertical integration plays, delivery platform buildouts, technology-forward dispensary concepts - many have attracted capital on narrative alone. Some have delivered. Many have not.

What Green Cross Health's profile illustrates is simpler: a licensed cannabis retail business that generates consistent profit, grows earnings, holds its margins, and is run by people with real money on the table is a fundamentally different risk proposition than a well-funded operator still searching for its path to profitability. For B2B suppliers, technology vendors, and institutional investors evaluating the cannabis retail space, that distinction isn't incidental. It's the whole argument.